This post may contain affiliate links. Please see my advertiser disclosure for more details.

Recently, Ken and I have been tinkering with some new ideas for being a bit more aggressive with our finances. Right now, the only investment accounts we have are our retirement accounts. We have 401k’s, Rollover IRAs, and Roth IRAs (one each type of account for each of us, so six retirement accounts total). Besides our checking account for everyday bills, the rest of our money sits in a savings account that earns less than 1% APY.

While I was trying to figure out how much of our balances I should tinker with, I realized that I never had never actually figured out just how much we needed to keep in a quickly-accessible savings account in case of an emergency.

I’ve read that you should have about 6-8 months worth of expenses in an emergency fund. Since we live in an area where job opportunities abound, and since we both work in high demand fields, I think we’re safe in erring on the lower end of that boundary and having six months worth of expenses on hand. Heck, Ken literally found a new job in three weeks the last time he was looking.

Also, it’s tough to envision a scenario where both of us would be out of work at the same time. But, you never know when we both might be out of work for months due to a car accident or something.

So, here’s what we did.

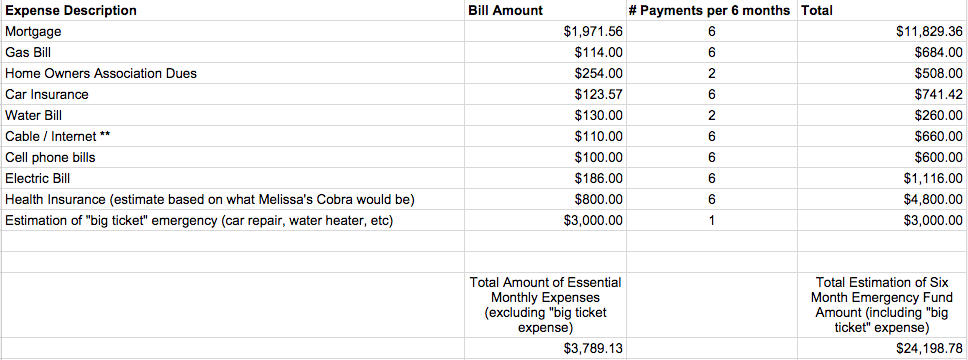

We figured out all of our monthly “necessity” expenses and their respective amounts. We then determined how frequently we would have to pay them in a six month period. For instance, our water bill and our Homeowners Association (HOA) dues are only paid quarterly. So in a six month period, we would only have to pay those bills twice.

{kind=link}

Then we multiplied each expense by the number of payments in a six month period, and then added up all of the expenses. To be extra cautious, we added an additional $3000 “big ticket emergency” expense, like a car repair or major home repair. We determined that we have $3789.13 in critical monthly expenses. Some expenses, like our cable and internet bill, we could likely decrease during unemployment by cutting out additional TV channels.

While this might be a bit controversial, I did not account for any day-to-day necessity expenses, like groceries or gas. The reason for this is I figure that unemployment insurance or short term disability insurance (offered by our employers) would be enough to cover our normal day-to-day expenses. And, like I mentioned earlier, it would be unlikely that both of us would be out of work at the same time, so presumably we would have at least one income to cover those day-to-day expenses. As a second option, if necessary, we could always dip into our Roth IRA accounts in an absolute dire circumstance since there are no penalties for withdrawal of the principal.

Since I carry the health insurance for both of us, paying for outside health insurance would only be an issue if I lost my job. We would probably be able to find something cheaper, but $800 is about what my COBRA insurance would cost (my contribution plus my employer’s contribution to my existing health insurance).

I did not account for any student loan payments because those are easily deferred during unemployment. Luckily our student loan payments are very reasonable, so hopefully we could continue to pay them, but it is nice to know that the payments can be deferred.

One thing that might need to be added to our calculations in the (somewhat) near future, is a car payment. Both of our cars are paid off. My car is 15 years old and has 102,000 miles on it. I plan on running it until it dies, and who knows when that could be. So, when I buy a new car, I’ll have to be sure to adjust the emergency fund calculations to account for a car payment.

So, according to the calculations, we should have $24,198.78 in an emergency fund. Let’s just call it $25,000 to make it a nice round number.

That leaves us with all our balances greater than $25,000 to be more aggressive with. Will we use every last penny of those remaining balances? Nope, we’re way too cautious for that. But, our emergency fund calculation does give us a good idea of what we need to keep untouched.

We’ll talk more about our ideas for those balances in future posts!